{kind=link}

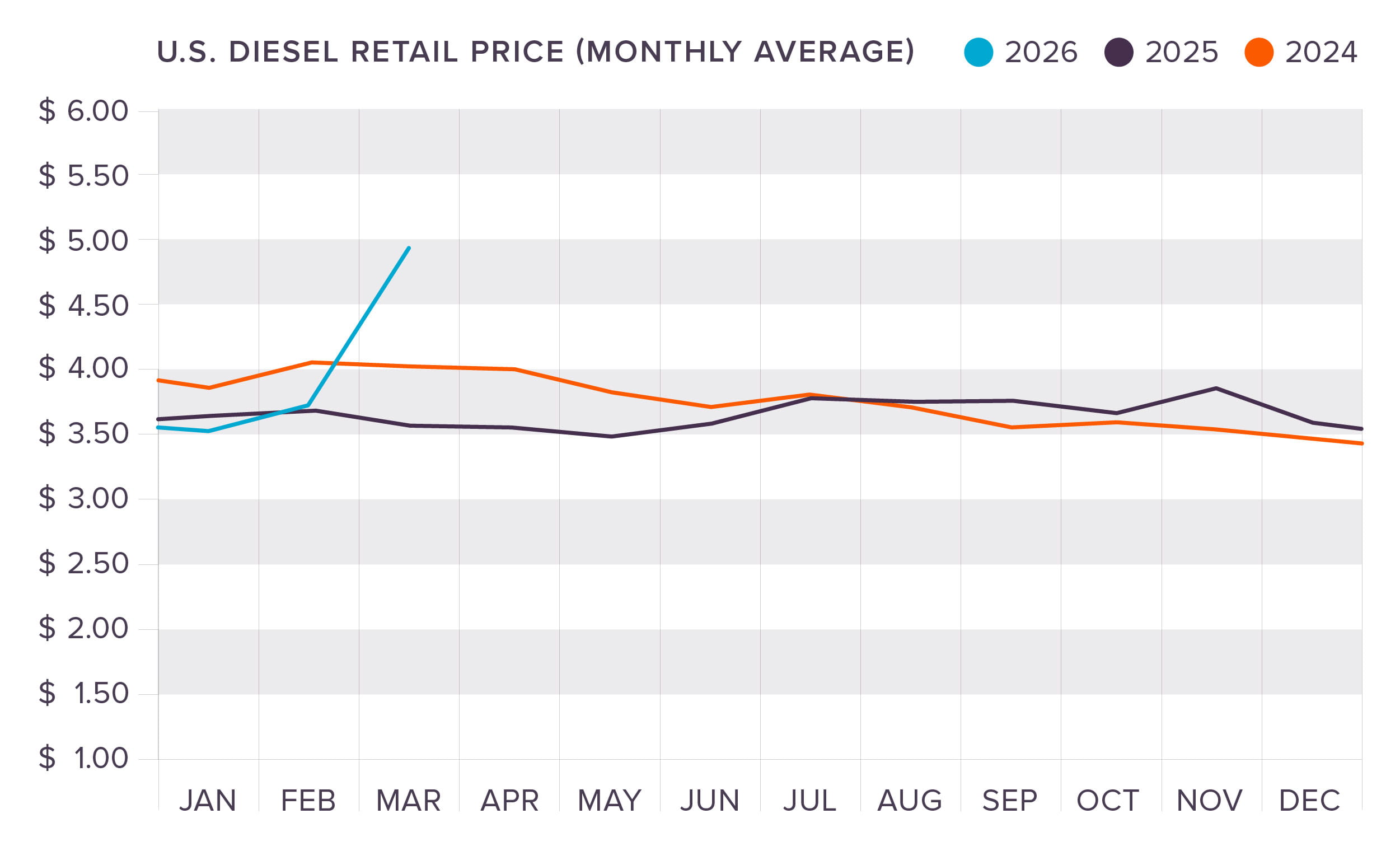

Q1 started with a freight market finally showing signs of life. It closed with a tariff-driven fuel price spike that changed the cost conversation. Diesel that opened the year around $3.50 per gallon, crossed $5.40 by the end of March. Freight rates climbed across all modes. Tonnage hit a three-year high. For shippers, the central question entering Q2 is whether their transportation strategy is built for the market they are in now.

Catch up on the Q4 2025 Data

Read the Q4 2025 Logistics Industry Report.

Growth Slows but Stays Positive

According to the Federal Reserve Bank of Atlanta’s GDPNow model, estimated real GDP growth is at 1.3 percent as of April 9. Growth has decelerated from the strong back half of 2025. Underlying demand has not stalled, but the moderation is real and relevant for shippers modeling freight volumes into Q2.

Consumer Confidence and Employment

The Consumer Confidence Index ticked up 0.8 points in March to 91.8, its highest reading of 2026. The unemployment rate held at 4.3 percent in March with 178,000 nonfarm payroll jobs added. Transportation and warehousing contributed 21,000 of those gains.

According to the Federal Reserve’s Industrial Production report, manufacturing output rose 0.7 percent in January and another 0.2 percent in February. Total industrial production stood 1.4 percent above year-earlier levels, and capacity utilization held steady at 76.3 percent.

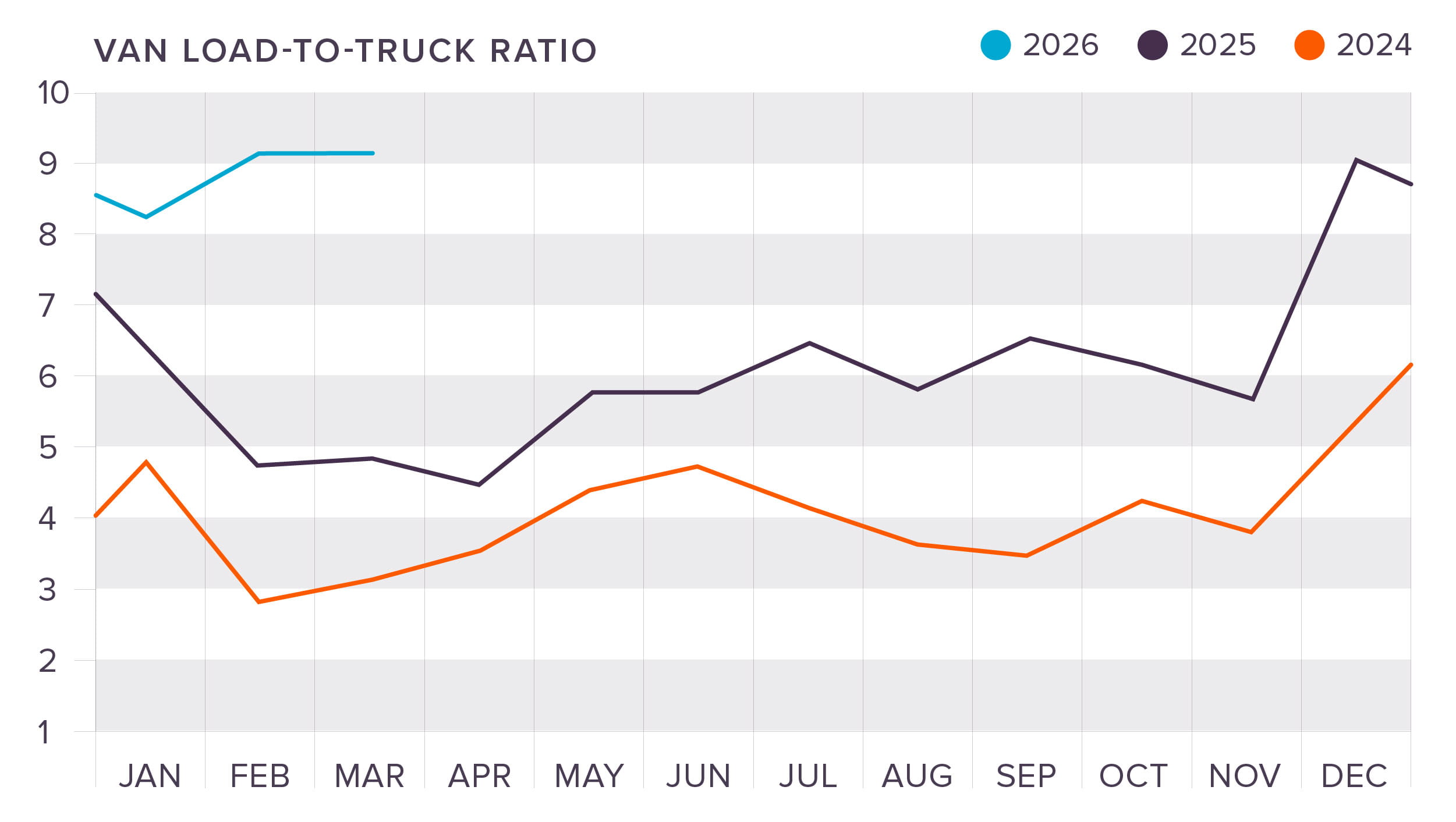

Van Capacity Tightens as the Market Turns

After spending most of the past two years oversupplied, the freight market entered Q1 in noticeably tighter shape. DAT Freight & Analytics reports the van load-to-truck ratio closing Q1 above 5.5 loads per available truck, signaling real competition for capacity.

National spot and contract rates at the close of Q1 2026:

- Van: $2.52 (Spot) | $2.72 (Contract)

- Flatbed: $3.09 (Spot) | $3.43 (Contract)

- Reefer: $2.98 (Spot) | $3.09 (Contract)

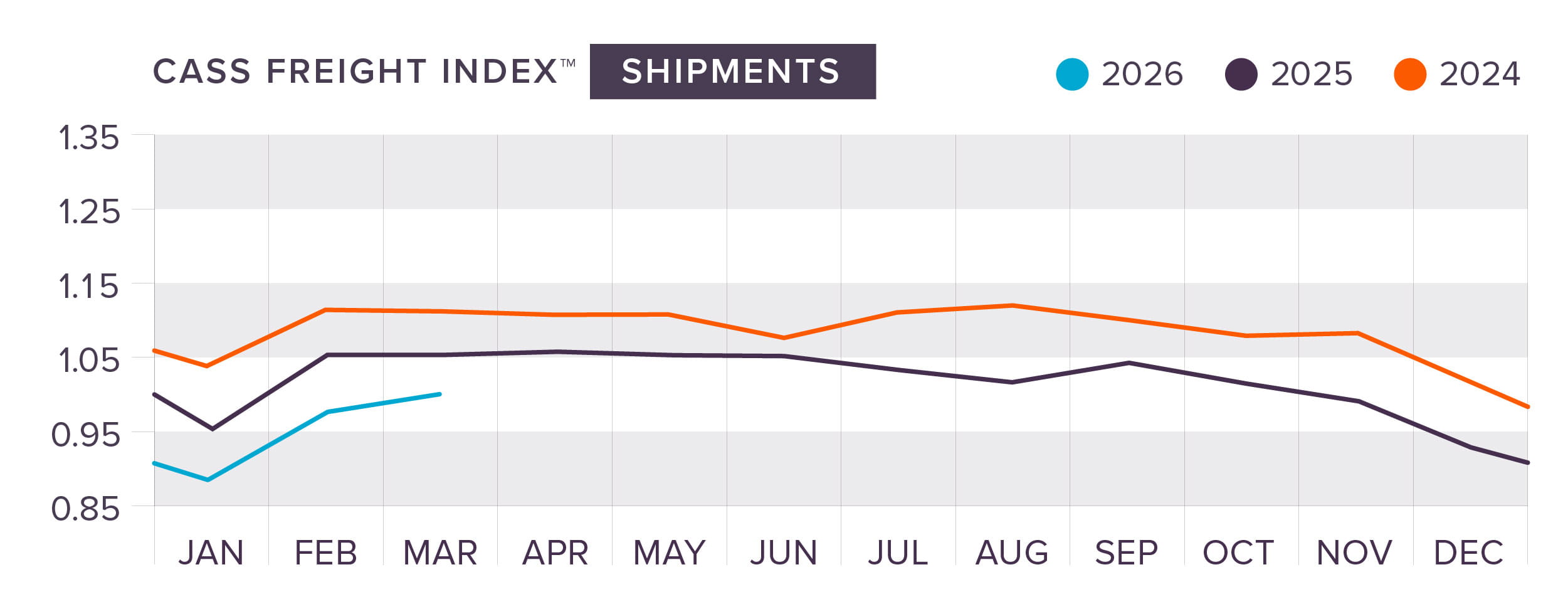

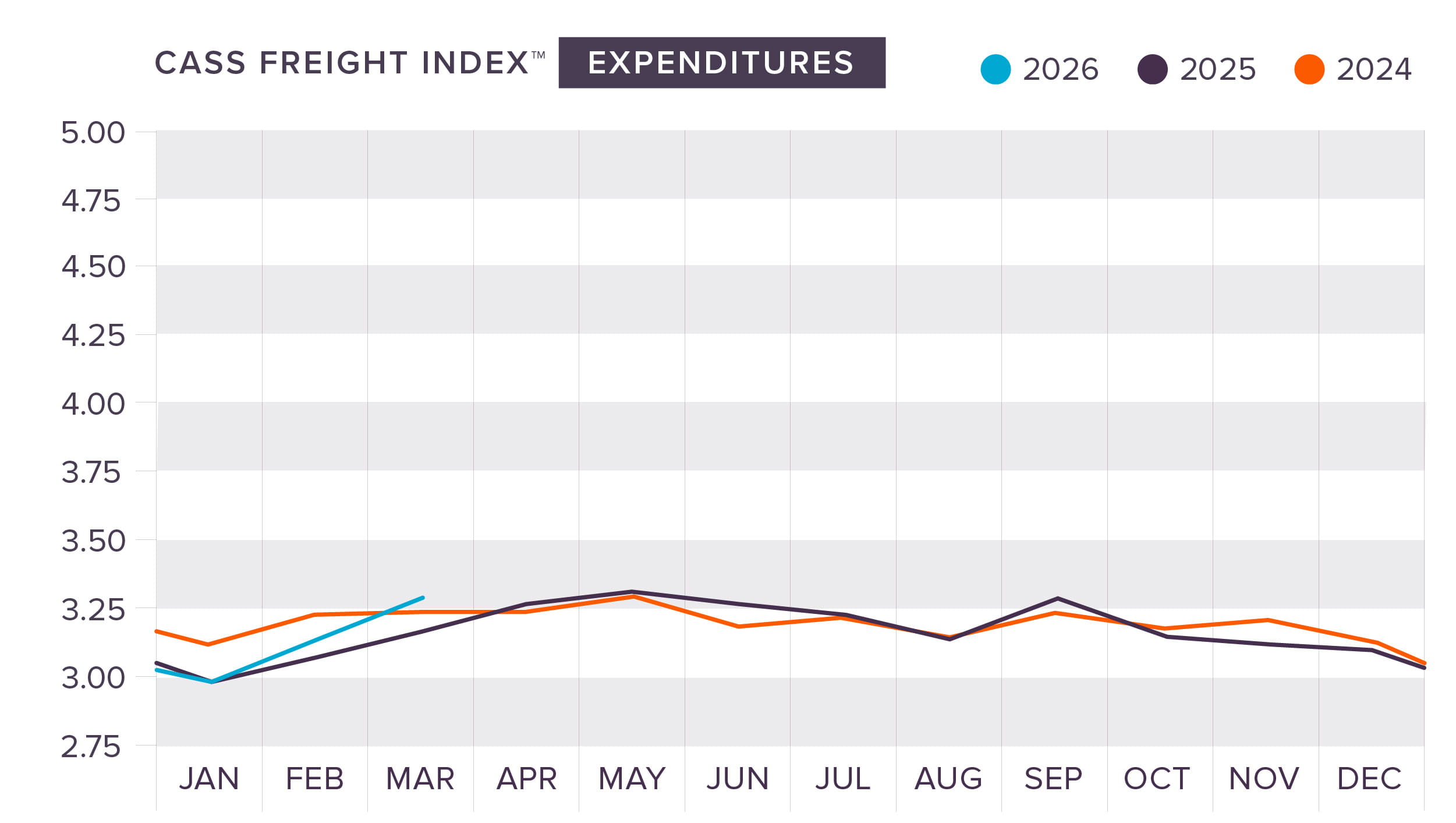

Freight Expenditures Rise as Shipment Volumes Slowly Recover

The Cass Freight Index reported two encouraging trends in Q1. Freight expenditures rose 4.2 percent year-over-year in March, accelerating from a 2.1 percent gain in February. Shipment volumes fell 4.5 percent year-over-year in March but rose 3.0 percent month-over-month, building on a 10.4 percent month-over-month gain in February.

Tonnage Hits a Three-Year High

The ATA Truck Tonnage Index surged 2.6 percent in February to 116.2 after a 0.7 percent gain in January. This is the highest level since early 2023 and the largest year-over-year gain since October 2022. Through the first two months of 2026, tonnage is running 1.4 percent above the same period last year. A meaningful acceleration after 2025’s full-year index came in flat.

Diesel Prices Surge in March

Diesel held relatively steady throughout January and February. Then March arrived. Prices jumped from $3.89 in the first week to $5.40 by month’s end and reached $5.64 as of the first week of April. That is a more than $2.00 increase in under three months. Fuel surcharges are adjusting to reflect the new reality, and shippers should expect those increases to show up in Q2 freight costs regardless of what happens to underlying rates.

Keep Moving with King

Q1 set a tone: capacity is tighter, fuel costs are higher, and the freight market is moving faster than most budgets anticipated. Shippers with structured strategies and strong carrier relationships are better positioned to absorb what Q2 brings. Those without them are already behind.

Now is the time to pressure-test your transportation strategy for what’s ahead. Contact King Solutions to start the conversation.