If you’ve read our prior reports for the year, you could largely describe them as a mixed bag. Some data brought good news; others lagged for months on end. We are happy to report that Q3 of 2024 looks to be the strongest yet. Nearly every metric shows good news for the logistics industry heading into the holiday season. While growth was modest, there is nothing ominous looming over the industry as we head into Q4.

Ready to look at the numbers? See the latest from the economy and the logistics industry!

Catch up on the Q2, 2024 Data

Want to see how the year started? Read our Q2 2024 Logistics Industry Report.

Expected Economic Growth Slows

As we head into the later months of the year, the expected Q3 Economic Growth is predicted to be 1.8%, which is an increase over prior forecasts. This reflects stronger spending, higher savings, and a healthier labor market. Overall, expected GDP growth for the entirety of 2024 currently sits at 2.4%.

Consumer Confidence Peaks and Jobs are Strong, Despite Falling Manufacturing Output

While optimism dipped in Q2, consumer confidence peaked in the late summer and early fall months. The Consumer Confidence Index grew to its highest level in a year, increasing to 41 percent from 33 percent. In the most recent survey, consumers indicated they planned to increase their spending on most essential, semi-discretionary, and discretionary items over the next three months, according to Mckinsey. While this confidence is welcoming, consumers still remain cautious about the economy overall. While consumers are cautious, they are also feeling some relief as inflation dropped to 2.4%, closer to the Federal Reserve’s goal of 2.0%.

The latest Jobs Report also brought some good news, with 254,000 nonfarm payroll jobs coming in September. The unemployment rate changed slightly at 4.1%. While these job numbers are great for the economy overall, there was little change in the total number of retail, manufacturing, and transportation industry jobs.

Manufacturing output was the only metric that struggled in Q3, falling by 0.6% in July, rebounding by 0.3% in August, and falling again by 0.4% in September. The Fed estimates that industrial production has declined by 0.6% in total over the past year.

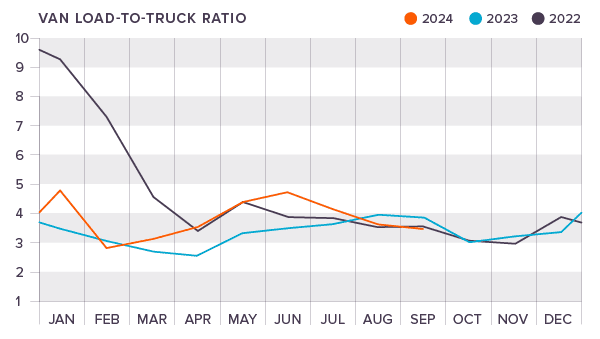

Capacity Loosens after a Tight Q2

The DAT Van Load-to-Truck Ratio showed heavy signs of relief as capacity became far more available in Q3 when compared to Q2. After peaking for the year in June with a Van Load-to-Truck Ratio of 4.72, the ratio dropped for three consecutive months (4.11 in July, 3.63 in August, and 3.49 in September), showing that there is much more capacity available in the market as we head into Q4.

National Spot and Contract Rates at the end of September were:

- Van: $1.97 (Spot) and $2.39 (Contract)

- Flatbed: $2.38 (Spot) and $3.04 (Contract)

- Reefer: $2.38 (Spot) and $2.73 (Contract)

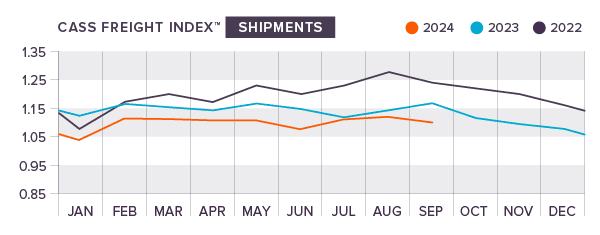

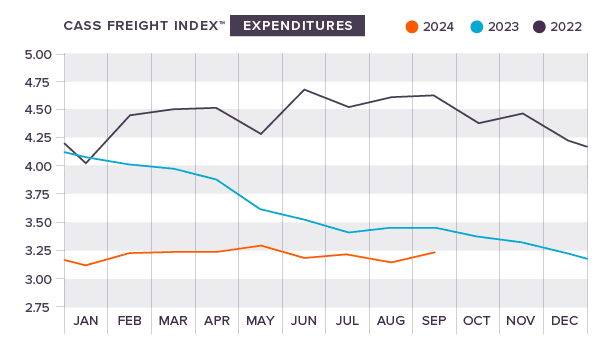

Freight Expenditures and Shipments Waver

The Cass Freight Index® for shipments and expenditures had a promising start in Q3, with shipments increasing by 3.1% m/m in July and 1.1% m/m in August. Expenditures also increased in July (0.7%) and fell in August (2.0%), leading to a decrease in truckload rates for the first two months. In September, the shipments index fell 2.6% with expenditures rising by 2.4%. This sudden turn erased some of the gains made in July and August, but the trendlines are showing some stability heading into the holiday season.

Read the September Cass Report

Tonnage Turns a Corner in Q3

The American Trucking Associations advanced seasonally adjusted For-Hire Truck Tonnage Index showed remarkable strength in Q3, finally turning a corner after struggling for much of the year. After dropping for multiple consecutive months in Q2, the ATA’s Tonnage Index increased 0.3%, a small increase that was kicked off by strong import activity and small growth in retail activity and factory output. The index exploded in August, increasing 1.8% and bringing the tonnage levels to their highest level since February of 2023. While the index still lags behind last year, this turn could kick off sequential months of growth that could remain for the rest of the year.

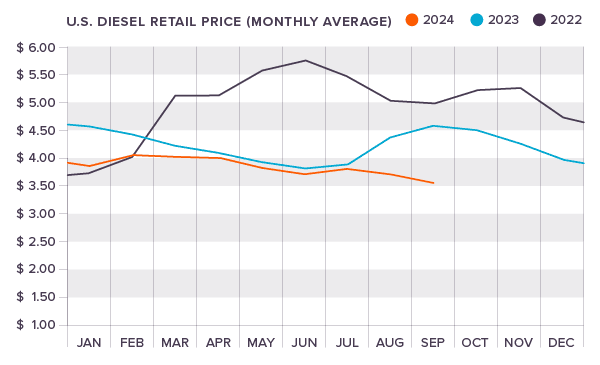

Diesel Fuel Prices Trend in the Right Direction

Nationwide diesel fuel prices continued to drop and provide relief for carriers and shippers throughout Q3, dropping from 3.813 at the start of July to 3.544 by the end of September. Prices have stabilized since peaking in February, and are down by almost a dollar since the same time last year.

As of the writing of this report, diesel fuel prices are at 3.573 per gallon.

Start Planning for Next Year

What are your goals for 2025? It’s time to start planning, and we want to be a part of it! We want to talk about how you can optimize your supply chain, control your costs, and better serve your customers next year. Get in touch with us today to talk about the solutions that would best fit your business.

Joel Rice

Joel Rice